The FHA MIP is temporary, even with what you may have heard. The requirement to keep paying for mortgage insurance may be avoided for some homeowners by simply letting the policy lapse, while for others, this can only be accomplished via refinancing. As property prices continue to rise and mortgage rates remain low, more people are opting to refinance their mortgages. The elimination of FHA MIP is a significant undertaking, but if you have decided to do so, it is unquestionably feasible. If you are finding out how to remove mortgage insurance FHA? You've come to the right place.

What Is An FHA MIP?

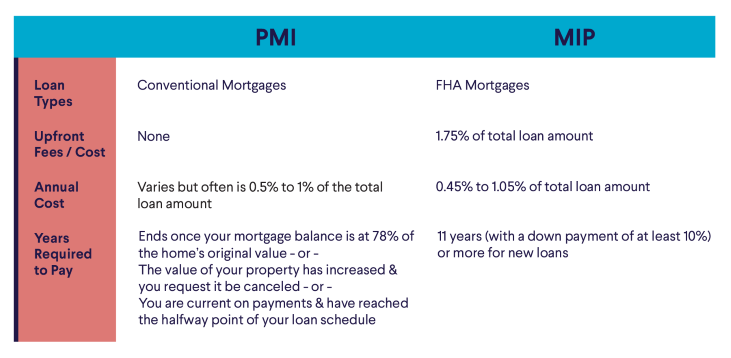

You may avoid defaulting on your FHA loan by purchasing FHA mortgage insurance. If this occurs and you are unable to repay your FHA loan, the FHA will cover the difference. The cost of this insurance is partially covered by the FHA MIP you and the more than 845,000 additional borrowers of FHA loans paid last year.

When may PMI be removed From An FHA Loan?

You have two options to choose from if you want to get rid of the yearly MIP on an FHA loan:

Wait until MIP runs out

Your FHA Mortgage Insurance Premium would be canceled after 11 years if you made a down payment of at least 10 percent of the home's purchase price.

Change Your Loan to a Traditional One

If you refinance your FHA loan into a conventional loan, you won't have to pay the MIP anymore. If you put just under 10 percent down on a home, this is your sole choice for canceling the FHA mortgage insurance premium.

Values of homes around the country are increasing, which is excellent news. Numerous FHA-insured homeowners have accrued sufficient equity to qualify for refinancing into a conventional loan, removing the need for mortgage insurance. Talk to a lender to see whether you qualify for an FHA loan cancellation.

Taking MIP out of an FHA Loan

Talk to your lender to find out whether you qualify for FHA MIP elimination and may therefore cease paying mortgage coverage on your FHA loan. To find out how to get rid of MIP on an FHA loan or how to remove FHA mortgage insurance, you should consider the aforementioned dates, which play a crucial role in the degree of adaptability of your loan terms. If your loan-to-value ratio (LTV) is greater than 79 percent (for loans originated between January 2001 & June 3, 2013), or if it's less than ten percent, you will have a hard time getting your FHA mortgage insurance canceled. However, you shouldn't discount the possibility of exploring other avenues, such as switching to a traditional loan through refinancing.

Eliminating the FHA Mortgage Insurance Premium through Refinancing

If your lender says the MIP cannot be removed, try refinancing to a traditional loan. Before committing to a refinancing, keep in mind the following details:

Credit score

How has your credit changed since you first applied for your FHA loan? Your hard work may pay off in the form of a traditional loan with a lower rate and no PMI if the loan-to-value (LTV) ratio is Eighty percent or less.

LTV ratio

The current worth of your house and how much you've paid toward your FHA loan are both important factors. To what extent do recent increases in home values or improvements to the property itself account for the increase in the home's market value?

Closing Costs

No, refinancing won't cost you anything. For the new loan, you will be responsible for paying various closing expenses, the total amount of which might reach several thousand dollars. Verify that refinancing will help you save a substantial amount of money and be worthwhile in the long term, in addition to eliminating your yearly MIP. You can get some guidance from Bankrate's mortgage refinancing calculator.

What Is The Cost Of MIP?

When you purchased your house, you also paid for an initial insurance policy known as the mortgage insurance premium (MIP). Your loan and the stack of documents you had to sign before you could take possession of your new house probably included an upfront MIP equivalent to 1.76 percent of the sum you borrowed. Your current payments are the second half of the MIP, the yearly MIP, and they are calculated depending on the specifics of your loan. Three primary elements determine the yearly MIP premium rates:

- Your loan's entire amount

- Your specified repayment period

- This is measured by the loan-to-value

Your yearly MIP will be anywhere from 0.45% to 1.050% of the loan principal, depending on the above variables.

- The 0.45% rate is for 15-year loans with above 10% equity.

- A loan term of more than 15 years and an outstanding balance of more than $624,500 would qualify for the 1.05 percent rate.

- Borrowers with less than a 5 percent down payment on a $624,500 or less 30-year FHA loan pay a yearly MIP of 0.87 percent.

Is It A Good Idea To Pay For PMI Or MIP?

To protect yourself financially, mortgage insurance is usually a good idea. The reason is with an FHA loan and MIP; you can put down a significantly lower amount on a property. Further, the credit requirements for FHA loans are more relaxed. If you can't get a mortgage minus mortgage coverage premiums, you may as well just pay them. Earlier on, you'll be able to begin amassing equity. Once you've saved 20% for a down payment, you'll be able to refinance into a traditional loan without having to pay private mortgage insurance. So, how to remove mortgage insurance on FHA loan is completely at your disposal.